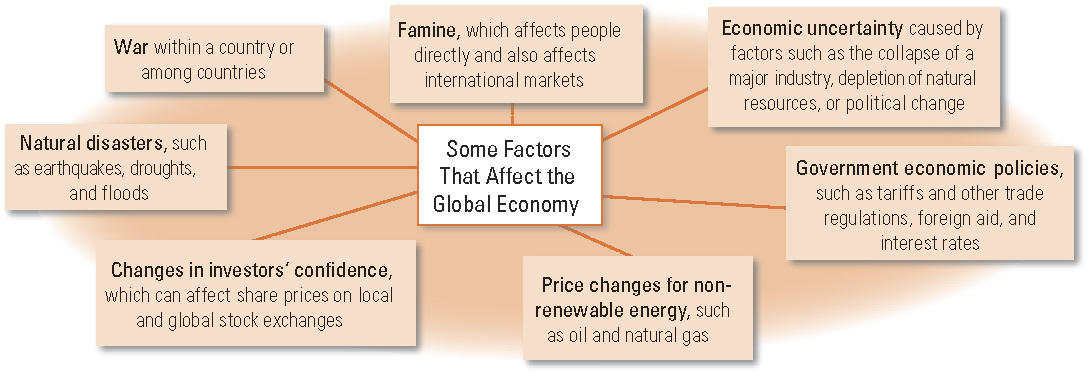

Economic Globalization

Key Terms: economic globalization, reparations, communism, economic depression, market economy

Focus #1

What does economic globalization mean?

What does economic globalization mean?

Economic Globalization is the spread of trade, transportation, and communication systems around the world in the interest of promoting worldwide commerce.

Economic Globalization includes the oil and gas pipelines and large tankers that carry oil products from Canada to markets around the world. It also affects the Canadian manufacturers who buy products and components from countries where workers are paid much less than Canadian workers.

Economic Globalization includes the oil and gas pipelines and large tankers that carry oil products from Canada to markets around the world. It also affects the Canadian manufacturers who buy products and components from countries where workers are paid much less than Canadian workers.

Focus #2

How did 20th century world events shape contemporary economic globalization?

How did 20th century world events shape contemporary economic globalization?

|

1914

World War 1 Begins

|

1917

Revolution and civil war begin in Russia

|

1918

World War 1 Ends

|

1922

Civil war ends in Russia with the Communist Party in control

|

|

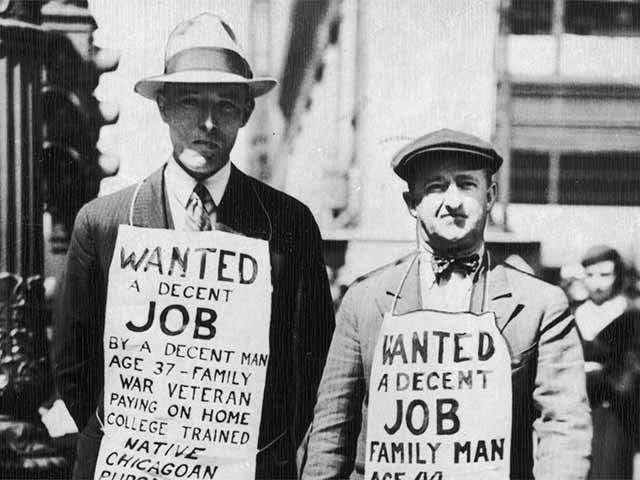

1929

Great Depression begins when stock markets crash in major cities

|

1939

World War 2 begins in Europe

|

1939-1941

Great Depression ends in various countries

|

1941

World War 2 expands to Asia when Japanese forces bomb Pearl Harbor and capture Hong Kong

|

| foundations_of_economic_globalization.pptx |

Focus #3

What factors laid the foundations of contemporary global economics?

What factors laid the foundations of contemporary global economics?

Bretton Woods

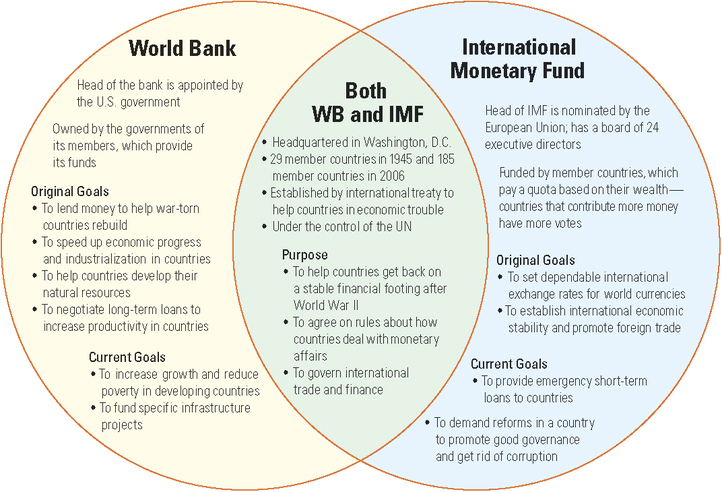

In July 1944, representatives of 44 countries met in the small New Hampshire town of Bretton Woods for a conference sponsored by the newly founded United Nations. World War II was not yet over - and would not end in Europe for another 10 months and in the Pacific for another 13 months. But conference delegates were already trying to figure out how they could prevent the kind of economic turmoil that could lead to another world war.

In July 1944, representatives of 44 countries met in the small New Hampshire town of Bretton Woods for a conference sponsored by the newly founded United Nations. World War II was not yet over - and would not end in Europe for another 10 months and in the Pacific for another 13 months. But conference delegates were already trying to figure out how they could prevent the kind of economic turmoil that could lead to another world war.

|

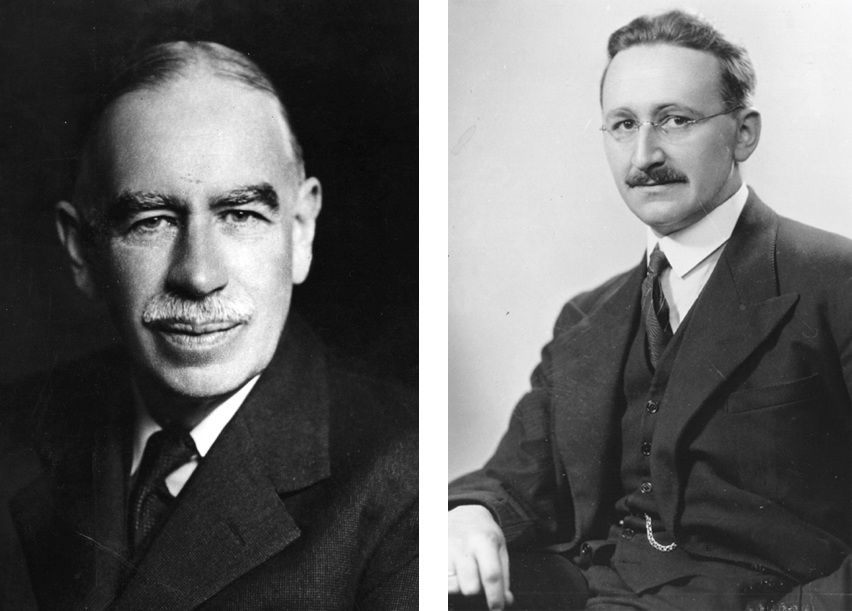

John Maynard Keynes

John Maynard Keynes, the British economist who had warned that the peace treaty that ended WW1 was doomed to fail, led the British delegation at Bretton Woods.

Keynes believed that the unrestricted capitalism that had existed before WW1 and between the two world wars had failed. He said that the collapse of global trade, the worldwide unemployment of the Great Depression, and the worst wars in history proved that the government's playing a very limited role in a country's economy was wrong. Keynes believed, for example, that when a business laid off workers because there was no market for its goods or services - as had happened during the Great Depression - governments should set up programs to hire the unemployed. He said that ensuring that people had money to spend would generate demand. Businesses would then need to rehire laid-off workers to produce more goods and services. |

John Maynard Keynes & Friedrich Hayek

|

General Agreement on Tariffs and Trade

At Bretton Woods, some countries agreed to work together to establish trade rules. This led to the General Agreement on Tariffs and Trade - GATT - which was signed in 1947. GATT members agreed to gradually eliminate tariffs and other trade barriers between themselves. Over the following decades, GATT representatives met many more time to lower tariffs and make trade freer.

The World Trade Organization - WTO - emerged from GATT in 1995. By 2007, the WTO was regulating trade in services, such as telecommunications and banking, as well as goods. It had also set rules to protect copyright and intellectual property, which refers to products of mind or intellect, such as slogans, industrial designs, communication technologies, and patents on drugs.

Market Economy: individuals were freer to make their own decisions with little intervention from the government - and where resources are the private property of individuals or companies (Public vs Private).

At Bretton Woods, some countries agreed to work together to establish trade rules. This led to the General Agreement on Tariffs and Trade - GATT - which was signed in 1947. GATT members agreed to gradually eliminate tariffs and other trade barriers between themselves. Over the following decades, GATT representatives met many more time to lower tariffs and make trade freer.

The World Trade Organization - WTO - emerged from GATT in 1995. By 2007, the WTO was regulating trade in services, such as telecommunications and banking, as well as goods. It had also set rules to protect copyright and intellectual property, which refers to products of mind or intellect, such as slogans, industrial designs, communication technologies, and patents on drugs.

Market Economy: individuals were freer to make their own decisions with little intervention from the government - and where resources are the private property of individuals or companies (Public vs Private).

| what_factors_laid_the_foundation_of_contemporary_global_economics.docx |